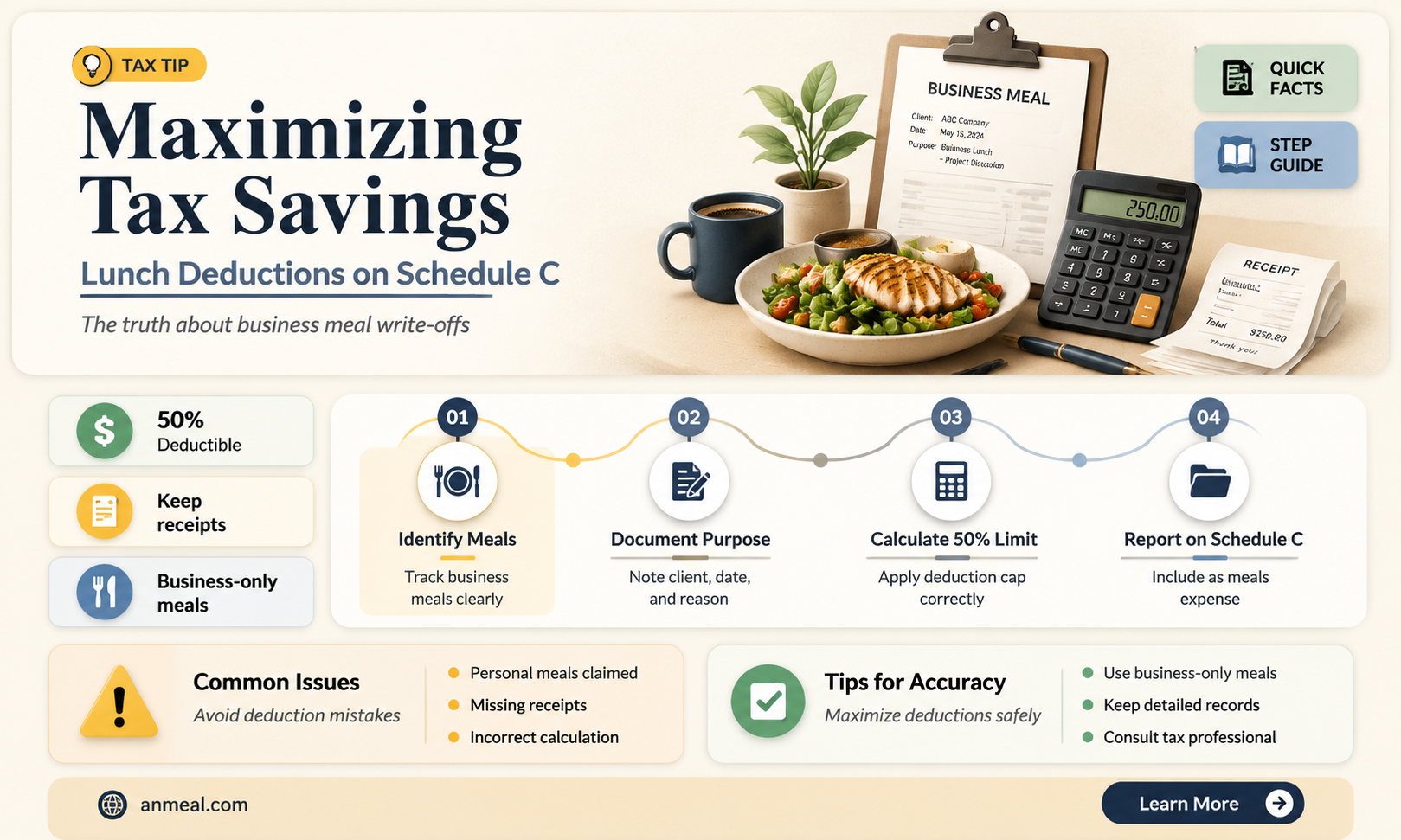

When it comes to tax deductions for business expenses, one common question that arises is whether lunches are deductible on Schedule C. Schedule C is the form used by sole proprietors to report their business income and expenses to the Internal Revenue Service (IRS). The good news is that business lunches can indeed be deductible, but there are certain rules and limitations that must be followed. Generally, the IRS allows deductions for business meals if they are considered ordinary and necessary expenses directly related to the conduct of your business. This means that the lunch must have a clear business purpose, such as discussing business matters with a client or potential client, or holding a meeting with business associates. Additionally, the amount of the deduction is limited to 50% of the actual cost of the meal. It's important to keep detailed records of your business lunches, including the date, location, attendees, and the business purpose of the meeting, in case of an audit. By following these guidelines, you can ensure that your business lunches are properly documented and eligible for deduction on your Schedule C.

Explore related products

What You'll Learn

- General Rule: Business lunches are partially deductible if they are ordinary and necessary expenses

- % Limitation: Only 50% of the cost of business lunches is deductible under Schedule C

- Documentation Requirements: Keep detailed records of the date, location, attendees, and business purpose

- Exceptions: Lavish or extravagant meals may not be deductible if they are not considered ordinary

- Tax Reform Changes: Recent tax reforms may have altered the deductibility rules for business meals

![]()

General Rule: Business lunches are partially deductible if they are ordinary and necessary expenses

To determine if business lunches are deductible on Schedule C, it's essential to understand the IRS's stance on meal expenses. The general rule is that business lunches are partially deductible if they are ordinary and necessary expenses. This means that the meal must be a typical expense incurred in the course of your business operations and not an extravagant or lavish expenditure.

When evaluating whether a business lunch meets the ordinary and necessary criteria, consider the following factors: the cost of the meal, the location, the attendees, and the business purpose. For instance, a meal at a mid-range restaurant with a client to discuss business matters would likely be considered ordinary and necessary. On the other hand, a meal at an upscale restaurant with no clear business purpose would not meet the criteria.

It's also important to note that the IRS has specific rules regarding the deductibility of meal expenses. For tax years 2018 through 2025, the Tax Cuts and Jobs Act (TCJA) allows for a 50% deduction for business-related meals, including business lunches. However, this deduction is only available if the meal is not considered a form of entertainment.

To ensure that your business lunches are deductible, it's crucial to maintain accurate records. This includes keeping track of the date, location, attendees, business purpose, and cost of the meal. By doing so, you can provide the IRS with the necessary documentation to support your deduction in case of an audit.

In summary, business lunches can be partially deductible on Schedule C if they are ordinary and necessary expenses. By understanding the IRS's criteria and maintaining accurate records, you can take advantage of this deduction to reduce your taxable income.

Charming in the Cafeteria: A Lunch Lady's Guide to Cute

You may want to see also

Explore related products

![]()

50% Limitation: Only 50% of the cost of business lunches is deductible under Schedule C

The 50% limitation on the deductibility of business lunches under Schedule C is a critical aspect of tax planning for small business owners and self-employed individuals. This rule means that only half of the expenses incurred for business-related meals can be claimed as a deduction on your tax return. Understanding this limitation is essential for maximizing your tax savings while ensuring compliance with IRS regulations.

To navigate this limitation effectively, it's important to keep detailed records of all business lunch expenses. This includes the date, location, amount spent, and the business purpose of each meal. Maintaining accurate documentation will help you substantiate your deductions in case of an audit and ensure that you're only claiming the allowable 50% of your expenses.

One strategy to optimize your deductions under this rule is to carefully plan your business lunches. For instance, consider scheduling meetings over lunch rather than dinner, as lunch is typically less expensive. Additionally, be mindful of the venues you choose; opting for less costly restaurants or cafes can help keep your expenses in check.

Another key consideration is the distinction between business and personal expenses. The IRS scrutinizes deductions that appear to blur the lines between personal and professional activities. To avoid raising red flags, ensure that your business lunches are clearly tied to a legitimate business purpose and that you're not mixing personal and business expenses on the same receipt.

In conclusion, while the 50% limitation on business lunch deductions under Schedule C may seem restrictive, there are strategies you can employ to make the most of this tax rule. By keeping meticulous records, planning your meals strategically, and maintaining a clear separation between personal and business expenses, you can maximize your deductions while minimizing the risk of IRS scrutiny.

Chill Your Sack Lunch: Tips for Keeping It Cold All Day

You may want to see also

Explore related products

![]()

Documentation Requirements: Keep detailed records of the date, location, attendees, and business purpose

To ensure that business lunches are deductible on Schedule C, it is crucial to maintain meticulous documentation. This involves keeping detailed records of the date, location, attendees, and business purpose of each lunch meeting. The date and location are essential for establishing the time and place of the business activity, while the attendees list helps identify the individuals involved in the meeting. Clearly stating the business purpose is key to demonstrating that the lunch was a legitimate business expense rather than a personal or social event.

When documenting the business purpose, it is important to be specific and detailed. Simply stating "business meeting" may not be sufficient. Instead, describe the topics discussed, the goals of the meeting, and how the lunch contributed to the overall business strategy. This level of detail helps substantiate the deduction and provides a clear paper trail in case of an audit.

In addition to these core elements, it is advisable to include other relevant details in your documentation. For example, you may want to note the duration of the meeting, the cost of the lunch, and any other expenses incurred during the event. Keeping receipts and invoices for the meal can also serve as valuable supporting documentation. By maintaining comprehensive and organized records, you can ensure that your business lunches are properly documented and more likely to be deductible on Schedule C.

Remember, the key to successful documentation is consistency and attention to detail. Make it a habit to record the necessary information immediately after each lunch meeting while the details are still fresh in your mind. This practice not only helps with tax compliance but also provides a useful record of your business activities and relationships.

Buttered Bliss: Microwaving Popcorn in a Lunch Bag Made Easy

You may want to see also

Explore related products

![]()

Exceptions: Lavish or extravagant meals may not be deductible if they are not considered ordinary

The IRS has specific guidelines regarding the deductibility of meals, including lunches, on Schedule C. While many business-related meals can be deducted, there are exceptions for lavish or extravagant meals that are not considered ordinary. This means that if you're a small business owner or self-employed individual, you need to be careful when claiming deductions for your meals.

To determine whether a meal is considered lavish or extravagant, the IRS looks at several factors, including the cost of the meal, the location, and the type of food served. For example, a meal at a high-end restaurant with expensive dishes and drinks may be considered lavish, while a meal at a casual diner would likely be considered ordinary. Additionally, the IRS considers the purpose of the meal. If the meal is for a business meeting or discussion, it is more likely to be deductible than a meal for personal reasons.

It's important to keep detailed records of your meals, including receipts and notes about the purpose of the meal, in case of an audit. This will help you prove that your meal deductions are legitimate and not for lavish or extravagant meals. You should also be aware of the IRS's rules regarding the percentage of meal expenses that can be deducted. Currently, the IRS allows deductions for 50% of business-related meal expenses.

In conclusion, while lunches can be deductible on Schedule C, it's important to be mindful of the IRS's rules regarding lavish or extravagant meals. By keeping detailed records and understanding the guidelines, you can ensure that your meal deductions are legitimate and avoid any potential issues with the IRS.

Exploring Local Delights: A Guide to Perfect Lunch Spots Nearby

You may want to see also

Explore related products

![]()

Tax Reform Changes: Recent tax reforms may have altered the deductibility rules for business meals

Recent tax reforms have significantly altered the landscape of business meal deductions, particularly impacting those reported on Schedule C. Prior to these changes, business owners could deduct 50% of their business-related meal expenses. However, the Tax Cuts and Jobs Act (TCJA) of 2017 introduced substantial modifications to these rules, affecting how business meals are reported and deducted.

One of the key changes is the elimination of the direct deduction for business meals. Instead, these expenses are now categorized as "entertainment expenses," which are subject to a 50% limitation. This means that only half of the cost of a business meal can be deducted, and the other half is considered a nondeductible expense. This shift has implications for how business owners track and report their meal expenses, as they must now ensure that their records clearly distinguish between the business and personal components of any meal.

Another important aspect of these reforms is the introduction of new rules for substantiating business meal expenses. To qualify for a deduction, business owners must provide clear and convincing evidence that the meal was business-related. This includes documenting the date, time, location, and purpose of the meal, as well as the names of the individuals present. Failure to provide adequate substantiation can result in the disallowance of the deduction.

The TCJA also expanded the definition of "business meals" to include expenses incurred while traveling for business. This means that business owners can now deduct 50% of their meal expenses while on business trips, provided they meet the substantiation requirements. This change is particularly beneficial for those who frequently travel for work, as it allows them to recover a portion of their meal costs.

In conclusion, the recent tax reforms have brought about significant changes to the deductibility of business meals on Schedule C. Business owners must now navigate a more complex set of rules and requirements to ensure they are maximizing their deductions while remaining compliant with the law. By understanding these changes and maintaining accurate records, business owners can continue to benefit from the tax advantages of business meal deductions.

Easy Steps to Clean and Maintain Your Insulated Lunch Bag

You may want to see also

Frequently asked questions

Yes, business lunches are generally deductible on Schedule C as a business expense. However, the deduction is limited to 50% of the cost.

A business lunch must be directly related to your business and conducted with a business associate, client, or potential client. It should be a bona fide business discussion or meeting.

If the primary purpose of the meeting is business-related and you discuss business matters during the lunch, it can be deductible. However, if the meeting is primarily social, the deduction may not be allowed.

Yes, you should keep records that include the date, time, location, amount spent, and the business purpose of the lunch. Keeping receipts and documenting the business relationship of the attendees is also advisable.

Generally, the cost of your own lunch is not deductible as a business expense on Schedule C. However, if you're traveling for business and the lunch is an ordinary and necessary expense, it may be deductible.