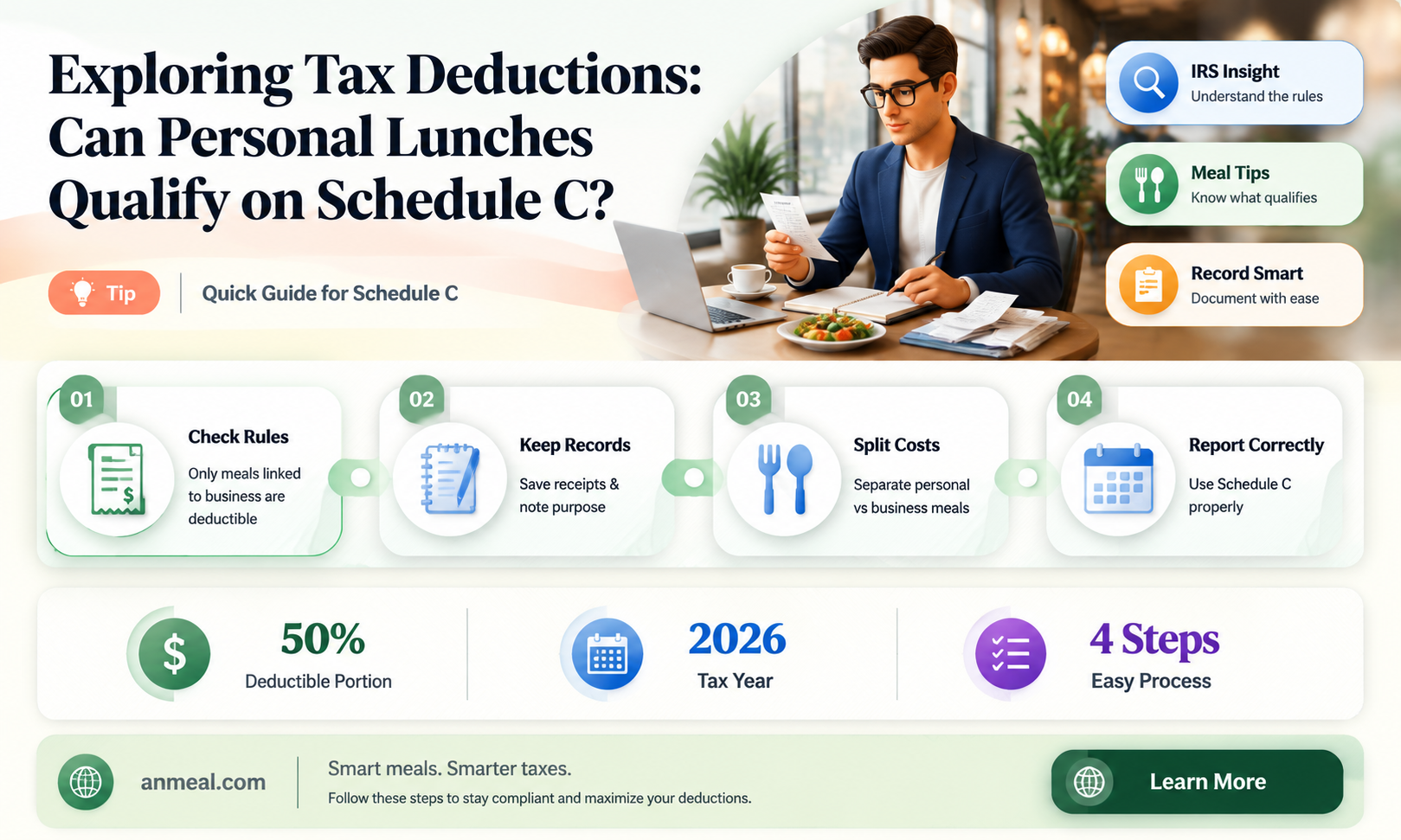

When it comes to tax deductions for personal lunches, the IRS has specific guidelines in place. Generally, personal meals are not deductible as they are considered a personal expense rather than a business one. However, there are exceptions to this rule, particularly for self-employed individuals or those operating a business. If a meal is directly related to the conduct of your business and you can substantiate the business purpose, it may be deductible. This includes meals with clients, colleagues, or business associates where the primary purpose is to discuss business matters. It's important to keep detailed records, including receipts and notes on the business purpose of the meal, to support any deductions you claim on Schedule C of your tax return.

| Characteristics | Values |

|---|---|

| Deduction Type | Business expense deduction |

| Schedule | Schedule C (Form 1040) |

| Eligibility | Self-employed individuals or sole proprietors |

| Purpose | Personal lunches related to business activities |

| Documentation Required | Receipts, invoices, or other supporting documents |

| Deduction Limit | Reasonable and necessary expenses only |

| Tax Year | Current tax year |

| Filing Status | Individual taxpayer |

| Business Type | Any business type (sole proprietorship, partnership, LLC, etc.) |

| Expense Category | Meals and entertainment |

| Record Keeping | Detailed records of dates, locations, and business purposes |

| IRS Scrutiny | Subject to IRS review and potential audit |

| Compliance | Must comply with IRS regulations and guidelines |

| Professional Advice | Recommended to consult a tax professional for guidance |

| Potential Benefits | Reduced taxable income, lower tax liability |

| Potential Drawbacks | Increased scrutiny, potential penalties for non-compliance |

Explore related products

What You'll Learn

- General Rule: Personal expenses, including lunches, are typically not deductible on Schedule C

- Business Purpose: If a lunch has a clear business purpose, such as meeting with a client, it may be deductible

- Documentation: Keeping detailed records of the business purpose and expenses is crucial for deduction eligibility

- Percentage Limitations: Even with a business purpose, only a certain percentage of meal expenses may be deductible

- IRS Guidelines: The IRS provides specific guidelines on what constitutes a deductible business expense for meals

![]()

General Rule: Personal expenses, including lunches, are typically not deductible on Schedule C

The general rule regarding personal expenses, including lunches, is that they are typically not deductible on Schedule C of your tax return. This is because Schedule C is designed to report business income and expenses, and personal expenses are generally not considered business-related. Therefore, it's important to understand what constitutes a personal expense versus a business expense to ensure you're not incorrectly claiming deductions.

One key factor in determining whether a lunch expense is deductible is the purpose of the meal. If the lunch is purely for personal enjoyment or convenience, it is not deductible. However, if the lunch is for business purposes, such as meeting with a client or discussing business matters with a colleague, it may be deductible. The IRS requires that the expense be "ordinary and necessary" for your business. This means that the lunch must be a common and reasonable expense in the context of your business activities.

To ensure that your lunch expenses are deductible, it's crucial to maintain proper documentation. This includes keeping receipts for the meal, noting the date, location, and amount of the expense, and providing a brief description of the business purpose of the lunch. Additionally, you should be aware of the IRS's rules regarding the deductibility of meal expenses, which may change from year to year.

It's also important to note that there are some exceptions to the general rule. For example, if you are a sole proprietor or single-member LLC, you may be able to deduct a portion of your personal lunch expenses if they are incurred while you are actively engaged in business activities. However, this is a complex area of tax law, and it's advisable to consult with a tax professional to ensure you're complying with the rules.

In summary, while personal expenses, including lunches, are typically not deductible on Schedule C, there are exceptions for business-related meals. Proper documentation and an understanding of the IRS's rules are essential to ensure that you're correctly claiming deductions for your business expenses.

Discover Local Delights: Where to Find Lunchly Within 5 Miles

You may want to see also

Explore related products

![]()

Business Purpose: If a lunch has a clear business purpose, such as meeting with a client, it may be deductible

To determine if a lunch is deductible on Schedule C, it's essential to establish a clear business purpose. This means the meal must be directly related to your business activities, such as meeting with a client, discussing business strategies with a colleague, or attending a business-related seminar. The IRS scrutinizes deductions closely, so it's crucial to have a legitimate reason for claiming the expense.

One effective way to ensure your lunch is deductible is to document the business purpose thoroughly. Keep a record of the date, time, location, and attendees of the meal, as well as a brief description of the business discussion or activity that took place. This documentation will serve as evidence to support your deduction in case of an audit.

It's also important to note that the IRS has specific rules regarding the deductibility of meals and entertainment expenses. Generally, you can deduct 50% of the cost of a business meal, but there are exceptions and limitations. For example, if the meal is considered lavish or extravagant, the IRS may disallow the deduction entirely.

In addition to documenting the business purpose, you should also be mindful of the frequency and nature of your business lunches. While an occasional meal with a client or colleague is likely deductible, regularly claiming meals with the same individuals or for the same purpose may raise red flags with the IRS.

To avoid any potential issues, it's a good idea to consult with a tax professional or accountant who can provide guidance on the specific rules and regulations surrounding business meal deductions. They can help you navigate the complexities of the tax code and ensure that you're taking advantage of all the deductions you're entitled to, while also avoiding any potential pitfalls.

Exploring Mar-a-Lago: Public Access for Lunch Unveiled

You may want to see also

Explore related products

![]()

Documentation: Keeping detailed records of the business purpose and expenses is crucial for deduction eligibility

Maintaining meticulous records is paramount when it comes to substantiating the business purpose of expenses, especially in the context of personal lunches. The IRS scrutinizes deductions claimed on Schedule C, and without proper documentation, taxpayers may find themselves at risk of disallowed deductions or even penalties. To ensure compliance and maximize eligible deductions, it is essential to keep detailed records that clearly articulate the business purpose of each expense.

One effective approach is to maintain a contemporaneous log or journal that captures the specifics of each business lunch. This should include the date, location, attendees, and a clear description of the business discussion or purpose. Supporting documentation, such as receipts or credit card statements, should be attached to the log to provide a comprehensive record. Additionally, taxpayers should be mindful of the IRS's guidelines on substantiation, which require records to be kept in a manner that is legible, coherent, and easily retrievable.

Taxpayers should also be aware of the potential pitfalls of inadequate documentation. For instance, a common mistake is to rely solely on credit card statements or receipts without providing additional context or explanation. This can lead to disallowed deductions, as the IRS may not be able to discern the business purpose from the documentation provided. To avoid such issues, taxpayers should take the time to review their records regularly and ensure that they are complete, accurate, and up-to-date.

In conclusion, proper documentation is the cornerstone of deduction eligibility for personal lunches on Schedule C. By keeping detailed records that clearly articulate the business purpose of each expense, taxpayers can maximize their deductions while minimizing the risk of disallowed claims or penalties. It is essential to maintain a contemporaneous log or journal, attach supporting documentation, and regularly review records to ensure compliance with IRS guidelines.

Crunchy Delights: Mastering the Art of Keeping Bread Fresh for Lunch

You may want to see also

Explore related products

![]()

Percentage Limitations: Even with a business purpose, only a certain percentage of meal expenses may be deductible

Even when a meal expense is incurred for a legitimate business purpose, the IRS imposes a limit on the percentage of the expense that can be deducted. This limitation is crucial for self-employed individuals and small business owners who frequently entertain clients or conduct business over meals. Currently, the IRS allows taxpayers to deduct only 50% of meal expenses that are directly related to the conduct of their business. This means that if you take a client out for a $100 lunch, you can only deduct $50 of that expense on your Schedule C.

The percentage limitation applies to all meal expenses, regardless of whether they are for travel, entertainment, or other business purposes. It's important to note that this rule has been in place since 2018, when the Tax Cuts and Jobs Act (TCJA) was enacted. Prior to the TCJA, the deduction limit for business meals was 100%, but the new law reduced this to 50% in an effort to curb excessive spending and ensure that taxpayers are only deducting expenses that are truly necessary for their business operations.

To navigate this limitation effectively, it's essential to keep detailed records of all meal expenses, including the date, location, amount, and business purpose of each meal. This will help you to accurately calculate the deductible portion of your meal expenses and avoid any potential issues with the IRS. Additionally, it's a good idea to consult with a tax professional to ensure that you are taking advantage of all available deductions while staying within the boundaries of the law.

One strategy that some taxpayers use to maximize their meal deductions is to combine business and personal expenses into a single meal. For example, if you are traveling for business and decide to take your family out for dinner, you can deduct the portion of the meal that is attributable to your business activities. However, it's important to be careful with this approach, as the IRS may scrutinize your records to ensure that you are not inflating your business expenses.

In conclusion, while the percentage limitation on meal deductions can be challenging to navigate, it's an important aspect of tax law that all self-employed individuals and small business owners should be aware of. By keeping accurate records and consulting with a tax professional, you can ensure that you are taking advantage of all available deductions while staying within the boundaries of the law.

Tailoring Your O365 Page for Quick Launch Efficiency

You may want to see also

Explore related products

![]()

IRS Guidelines: The IRS provides specific guidelines on what constitutes a deductible business expense for meals

The IRS provides specific guidelines on what constitutes a deductible business expense for meals. To qualify as a deductible business expense, a meal must be directly related to the active conduct of your business. This means that the meal must have a clear business purpose, such as discussing business matters with a client or colleague. The IRS also requires that you keep detailed records of the meal, including the date, time, location, amount spent, and the business purpose of the meal.

One important aspect of the IRS guidelines is the distinction between entertainment and business expenses. While meals with clients or colleagues can be considered business expenses, the IRS has specific rules for deducting entertainment expenses, such as meals at restaurants or sporting events. Generally, entertainment expenses are only deductible if they are directly related to the active conduct of your business and if you are present at the event.

Another key consideration is the amount spent on the meal. The IRS has limits on the amount that can be deducted for business meals, and these limits vary depending on the circumstances. For example, if you are traveling for business, you may be able to deduct a higher amount for meals than if you are dining at home. It's important to keep track of your expenses and to consult with a tax professional to ensure that you are complying with the IRS guidelines.

In addition to the general guidelines, the IRS also has specific rules for deducting meals on Schedule C of your tax return. Schedule C is used to report income and expenses from a sole proprietorship or single-member LLC. When deducting meals on Schedule C, you must itemize your expenses and provide documentation to support your deductions. This can include receipts, credit card statements, or other records that show the amount spent and the business purpose of the meal.

Overall, the IRS guidelines for deducting business meals are complex and require careful attention to detail. By keeping accurate records and consulting with a tax professional, you can ensure that you are taking advantage of all the deductions available to you while staying in compliance with the IRS rules.

Efficiently Compiling Lunch Orders for Your Next Meeting

You may want to see also

Frequently asked questions

Generally, personal lunches are not deductible on Schedule C. Schedule C is used to report income and expenses related to a sole proprietorship or single-member LLC, and personal expenses are typically not considered deductible business expenses.

If the lunch is with a client or business associate and has a clear business purpose, then it may be considered a deductible business expense. You should keep records of the meeting, including the date, location, attendees, and the business topics discussed.

A lunch has a clear business purpose if it is directly related to the active conduct of your business. This could include discussing business strategies, negotiating contracts, or building relationships with clients or business associates. Personal or social conversations do not qualify as a business purpose.

For a deductible business lunch, you should keep a record that includes the date and location of the lunch, the names of the attendees, the business topics discussed, and the cost of the lunch. Keeping receipts and credit card statements can also help substantiate the expense.

If you work from home and eat at your desk, the cost of your lunch may be considered a personal expense and not deductible on Schedule C. However, if you can demonstrate that the lunch was a necessary part of your workday and not a personal choice, you may be able to deduct the cost as a business expense.