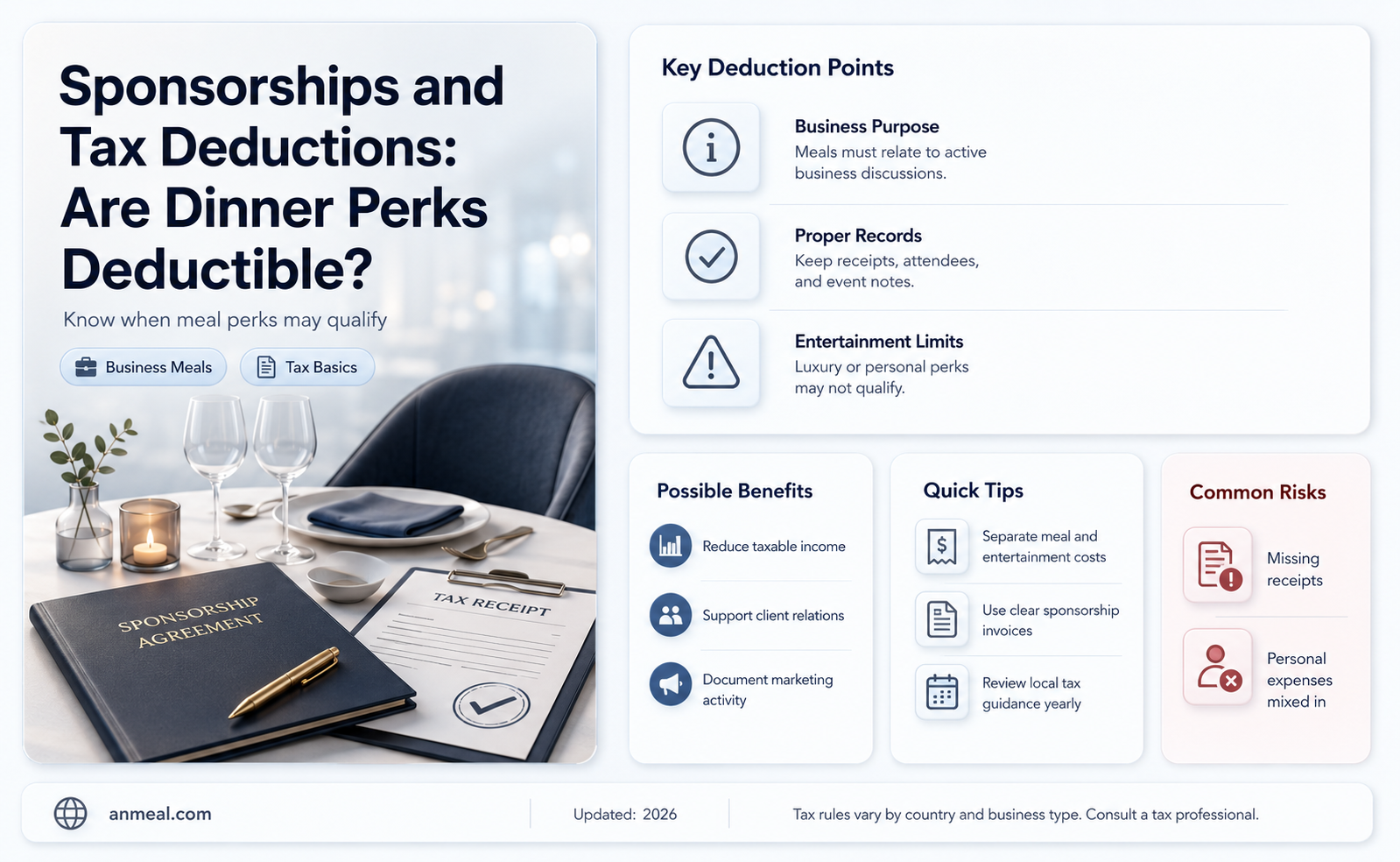

Sponsorships can be a valuable way for businesses to support events, organizations, or individuals while gaining exposure, but determining their tax deductibility can be complex. When a sponsorship includes perks like a dinner, the tax treatment becomes even more nuanced. Generally, the IRS allows businesses to deduct sponsorship expenses as ordinary and necessary business expenses, but the portion of the payment attributable to personal benefits, such as a meal, may not be deductible. To qualify for a deduction, the primary purpose of the sponsorship must be business-related, and the value of any goods or services received in return, including the dinner, must be carefully considered and potentially excluded from the deductible amount. Proper documentation and adherence to IRS guidelines are essential to ensure compliance and maximize potential tax benefits.

| Characteristics | Values |

|---|---|

| Tax Deductibility | Sponsorships may be tax-deductible if they meet specific IRS criteria. |

| Quid Pro Quo | If the sponsor receives a benefit (e.g., dinner), the deductible amount is reduced by the fair market value of the benefit. |

| Business Purpose | The sponsorship must have a clear business purpose (e.g., advertising, goodwill). |

| Documentation | Proper documentation of the sponsorship and benefits received is required. |

| Fair Market Value | The value of the dinner or other benefits must be reasonably estimated. |

| IRS Guidelines | Follow IRS Publication 526 and 535 for detailed rules on charitable contributions and business expenses. |

| Charitable vs. Business Sponsorship | If sponsoring a charity, the deductible amount is limited to the excess over the fair market value of benefits received. |

| Non-Cash Benefits | Non-cash benefits (e.g., dinner) are subject to specific valuation rules. |

| Reporting Requirements | Deductible amounts must be reported on the appropriate tax forms (e.g., Schedule C for businesses). |

| State Tax Laws | State tax laws may differ from federal rules, so check local regulations. |

Explore related products

$13.9 $25

$12.99 $15.99

What You'll Learn

- IRS Rules on Sponsorships: Understand IRS guidelines for deducting sponsorship expenses, including meals as benefits

- Business Purpose Requirement: Sponsorships must have a clear business purpose to qualify for deductions

- Meal Deduction Limits: Only 50% of meal expenses related to sponsorships are typically deductible

- Documentation Needed: Proper records of sponsorship agreements and meal expenses are essential for deductions

- Non-Profit vs. For-Profit: Tax rules differ for sponsorships of non-profits versus for-profit organizations

![]()

IRS Rules on Sponsorships: Understand IRS guidelines for deducting sponsorship expenses, including meals as benefits

Sponsorships can be a powerful tool for businesses to gain exposure and support causes, but the tax implications of these arrangements are often complex. The IRS has specific guidelines for deducting sponsorship expenses, particularly when meals are involved as benefits. Understanding these rules is crucial to ensure compliance and maximize tax benefits. For instance, the IRS generally allows businesses to deduct up to 50% of meal expenses associated with sponsorships, provided they meet certain criteria, such as being directly related to the business and properly documented.

To navigate these rules effectively, businesses must first distinguish between advertising expenses and sponsorships. While advertising costs are typically fully deductible, sponsorships may be subject to limitations, especially when they include perks like dinners. For example, if a company sponsors a local event and receives a dinner for its executives as part of the package, the deductibility of that meal depends on whether it is considered an entertainment expense or a business necessity. The IRS requires that such expenses be "directly related" to the active conduct of business, meaning there must be a clear business purpose for the meal.

One practical tip for businesses is to maintain detailed records of sponsorship agreements and associated expenses. This includes documenting the business purpose of meals, the attendees, and their relationship to the business. For instance, if a sponsored dinner includes potential clients or partners, the expense is more likely to be deductible. However, if the dinner is primarily social or personal in nature, the deduction may be disallowed. Additionally, businesses should be aware of the IRS’s substantiation requirements, which mandate written records within a reasonable time after the expense is incurred.

A comparative analysis reveals that sponsorships with meal benefits are treated differently than traditional business meals. While the Tax Cuts and Jobs Act of 2017 eliminated deductions for most entertainment expenses, business meals remain deductible at 50%. However, sponsorships complicate this rule because they often blur the line between entertainment and business. For example, a sponsored gala dinner may include both networking opportunities and entertainment elements. In such cases, businesses must carefully allocate expenses to comply with IRS guidelines.

In conclusion, businesses seeking to deduct sponsorship expenses, including meals, must adhere to strict IRS rules. By understanding the distinction between advertising and sponsorships, maintaining thorough documentation, and ensuring meals serve a clear business purpose, companies can navigate these complexities effectively. While the process may seem daunting, the potential tax benefits make it worthwhile for those who approach sponsorships strategically and with compliance in mind.

Understanding Dinner Services: A Guide to Elegant Table Settings and Etiquette

You may want to see also

Explore related products

![]()

Business Purpose Requirement: Sponsorships must have a clear business purpose to qualify for deductions

Sponsorships can be a powerful tool for businesses to gain exposure, build relationships, and support causes they care about. However, when it comes to tax deductions, not all sponsorships are created equal. The IRS requires that sponsorships have a clear business purpose to qualify for deductions. This means that simply donating money or resources in exchange for a dinner invitation won't cut it. The sponsorship must be directly related to your business's trade or profession, and the benefits received should be proportional to the amount spent.

For instance, consider a local restaurant sponsoring a charity gala. If the sponsorship includes a dinner for the business owner and the primary purpose is to entertain clients or foster business relationships, it may meet the business purpose requirement. However, if the dinner is merely a perk with no direct connection to the business's operations or marketing strategy, the IRS is unlikely to allow the deduction. To ensure compliance, businesses should document the sponsorship's objectives, expected benefits, and how it aligns with their overall business goals.

A comparative analysis of two scenarios can illustrate the importance of this requirement. In Scenario A, a tech company sponsors a tech conference where they will showcase their products, network with potential clients, and gain industry visibility. The sponsorship clearly serves a business purpose, making it deductible. In Scenario B, the same company sponsors a local sports team primarily because the owner’s child plays on it, with no direct business benefit. Here, the sponsorship lacks a clear business purpose and would likely be disallowed as a deduction. The distinction lies in whether the sponsorship directly advances the business's interests.

To navigate this requirement effectively, businesses should follow a structured approach. First, define the specific business objectives the sponsorship aims to achieve, such as brand exposure, lead generation, or community engagement. Second, ensure the sponsorship agreement explicitly outlines these objectives and the benefits the business will receive. Third, maintain detailed records, including invoices, contracts, and documentation of how the sponsorship contributed to business goals. Finally, consult a tax professional to verify that the sponsorship meets IRS criteria before claiming the deduction.

In conclusion, while sponsorships can offer valuable opportunities for businesses, their tax deductibility hinges on a clear business purpose. By aligning sponsorships with strategic business objectives and maintaining thorough documentation, companies can maximize their benefits while staying compliant with tax regulations. Ignoring this requirement risks not only the loss of deductions but also potential audits or penalties. Treat sponsorships as investments in your business, not just charitable gestures, and their value will extend far beyond the dinner table.

Warm Welcomes: Mastering the Art of Hosting Dinner Guests Gracefully

You may want to see also

Explore related products

![]()

Meal Deduction Limits: Only 50% of meal expenses related to sponsorships are typically deductible

Sponsorships often involve meals, but the tax deductibility of these expenses is not straightforward. One critical rule stands out: only 50% of meal expenses related to sponsorships are typically deductible. This limitation, rooted in IRS regulations, aims to balance the business value of such expenditures with the potential for personal benefit. For organizations and individuals navigating sponsorship agreements, understanding this cap is essential to avoid overclaiming deductions and facing audits.

Consider a scenario where a company sponsors a local event and hosts a dinner for key stakeholders. If the meal costs $1,000, only $500 can be deducted as a business expense. This 50% rule applies regardless of the meal’s purpose—whether it’s fostering client relationships, celebrating a partnership, or discussing sponsorship terms. The IRS views meals as partially personal, even in a business context, hence the reduced deductibility.

To maximize deductions within this limit, meticulous record-keeping is crucial. Document the business purpose of the meal, the attendees, and their relationship to the sponsorship. For example, if a dinner is held to finalize a sponsorship deal, note how the discussion advanced the agreement. Without clear documentation, the IRS may disallow the deduction entirely. Digital tools like expense-tracking apps can simplify this process, ensuring every detail is captured.

A common pitfall is treating the 50% rule as a one-size-fits-all solution. While it applies broadly, exceptions exist. For instance, meals provided for the greater good—such as those served at charitable events—may qualify for a higher deduction rate under specific IRS provisions. However, sponsorships rarely fall into this category, so relying on the 50% rule is generally safe. When in doubt, consult a tax professional to ensure compliance.

Finally, strategic planning can mitigate the impact of the 50% limit. For example, if a sponsorship involves multiple meals, consider structuring the agreement to include non-meal benefits, such as advertising or event naming rights. These expenses are often fully deductible, provided they are clearly separated from meal costs in the contract. By diversifying the sponsorship package, organizations can optimize their tax benefits while adhering to IRS guidelines.

Can Frozen Dinner Trays Be Recycled? A Comprehensive Guide

You may want to see also

![]()

Documentation Needed: Proper records of sponsorship agreements and meal expenses are essential for deductions

Sponsorships can indeed be tax-deductible, but the devil is in the details—specifically, the documentation. When a sponsorship includes a meal, such as a dinner, the IRS scrutinizes these arrangements to ensure they meet business purpose and substantiation requirements. Proper records are not just helpful; they are mandatory to avoid audits, penalties, or disallowed deductions. Without them, even legitimate expenses can be challenged, leaving businesses or individuals financially exposed.

To claim a deduction, start by securing a written sponsorship agreement that clearly outlines the terms, including the value of the sponsorship, the nature of the meal provided, and the business purpose of the arrangement. This document should explicitly state that the sponsorship is not contingent on the meal but rather supports a broader business objective, such as brand exposure or community engagement. For example, if a company sponsors a charity gala and receives a dinner as part of the package, the agreement must emphasize the primary purpose of supporting the charity, not the meal itself.

Next, maintain detailed records of meal expenses, including receipts, dates, attendees, and their business relationship to the sponsor. The IRS requires that meal expenses be "ordinary and necessary" for conducting business, so documentation should demonstrate a direct connection between the meal and a legitimate business activity. For instance, if a sponsored dinner includes potential clients or partners, note their names, titles, and the discussion topics to establish a clear business purpose. Failure to provide this level of detail can result in the expense being reclassified as entertainment, which is only 50% deductible under current tax laws.

Finally, cross-reference sponsorship agreements with financial records to ensure consistency. Discrepancies between the agreed-upon sponsorship value and the claimed deductions can raise red flags. For example, if a $5,000 sponsorship includes a $500 dinner, the deduction should reflect the total sponsorship amount, with the meal expense itemized separately. This approach not only satisfies IRS requirements but also provides a clear audit trail, reducing the risk of disputes. In essence, meticulous documentation transforms a potentially ambiguous expense into a defensible deduction.

Understanding Table d'Hôte: A Guide to Fixed-Menu Dining Experiences

You may want to see also

![]()

Non-Profit vs. For-Profit: Tax rules differ for sponsorships of non-profits versus for-profit organizations

Sponsorships can be a powerful tool for businesses and individuals to support causes or events while potentially gaining tax benefits. However, the tax deductibility of sponsorships, especially when they include perks like dinners, hinges on whether the recipient is a non-profit or for-profit organization. Understanding these differences is crucial for maximizing tax advantages while staying compliant with IRS regulations.

For non-profit organizations, sponsorships are generally treated as charitable contributions if they meet specific criteria. According to IRS guidelines, a payment to a non-profit can be deductible if the sponsor receives no substantial benefit in return. For instance, if a business sponsors a charity gala and receives only nominal benefits, such as logo placement or a brief acknowledgment, the entire sponsorship amount may be tax-deductible. However, if the sponsor receives a dinner or other significant benefits, the fair market value of those benefits must be subtracted from the sponsorship amount to determine the deductible portion. For example, if a $5,000 sponsorship includes a $500 dinner, only $4,500 would be deductible. Non-profits must provide sponsors with a written acknowledgment detailing the deductible amount, ensuring transparency and compliance.

In contrast, sponsorships of for-profit organizations are typically treated as advertising or marketing expenses, not charitable contributions. This means the entire sponsorship amount may be deductible as a business expense, but it is subject to different rules. For instance, if a business sponsors a for-profit event and receives dinner as part of the package, the cost of the dinner is considered a business entertainment expense. As of 2021, the Tax Cuts and Jobs Act (TCJA) eliminated the deduction for most entertainment expenses, but meals remain 50% deductible if they are directly related to the active conduct of business. Therefore, if a $1,000 sponsorship includes a $200 dinner, $100 of the meal expense would be deductible, and the remaining $900 would be fully deductible as a business expense.

A key takeaway is that the nature of the recipient organization—non-profit or for-profit—dictates the tax treatment of sponsorships. Non-profit sponsorships often allow for larger deductions but require careful valuation of benefits received. For-profit sponsorships, while fully deductible as business expenses, are subject to limitations on meal and entertainment deductions. To navigate these rules effectively, sponsors should maintain detailed records of sponsorship agreements, benefits received, and their fair market values. Consulting a tax professional can provide tailored advice, ensuring compliance and optimizing tax benefits.

Practical tips include negotiating sponsorship agreements that clearly outline benefits and their values, requesting written acknowledgments from non-profits, and separating meal expenses from other sponsorship costs for easier reporting. By understanding these distinctions, sponsors can strategically structure their contributions to align with their financial and philanthropic goals while adhering to IRS regulations.

Who Hosts Family Dinner? Traditions, Roles, and Modern Shifts

You may want to see also

Frequently asked questions

It depends. If the dinner is considered a benefit or goodwill gesture, the deductible amount may be reduced by the fair market value of the meal. Consult IRS guidelines or a tax professional for specifics.

No, businesses cannot claim a full deduction if the sponsorship includes a tangible benefit like a dinner. The deductible amount must exclude the value of the meal.

The deductible portion is calculated by subtracting the fair market value of the dinner from the total sponsorship amount. Only the remaining balance is eligible for a tax deduction.

Generally, no. However, if the dinner is incidental or minimal in value compared to the sponsorship, it may not affect deductibility. Always refer to tax regulations or seek professional advice.