When it comes to tax deductions for business expenses, one common question that arises is whether subcontractor lunches are deductible. This query often pertains to businesses that engage with independent contractors or subcontractors for various projects. Understanding the deductibility of these expenses is crucial for accurate tax reporting and maximizing allowable deductions. Generally, the IRS allows deductions for business meals if they are ordinary and necessary expenses directly related to the business. However, the rules can be nuanced, especially when it involves subcontractors. It's important to consider factors such as the nature of the relationship between the business and the subcontractor, the purpose of the meal, and the documentation supporting the expense.

Explore related products

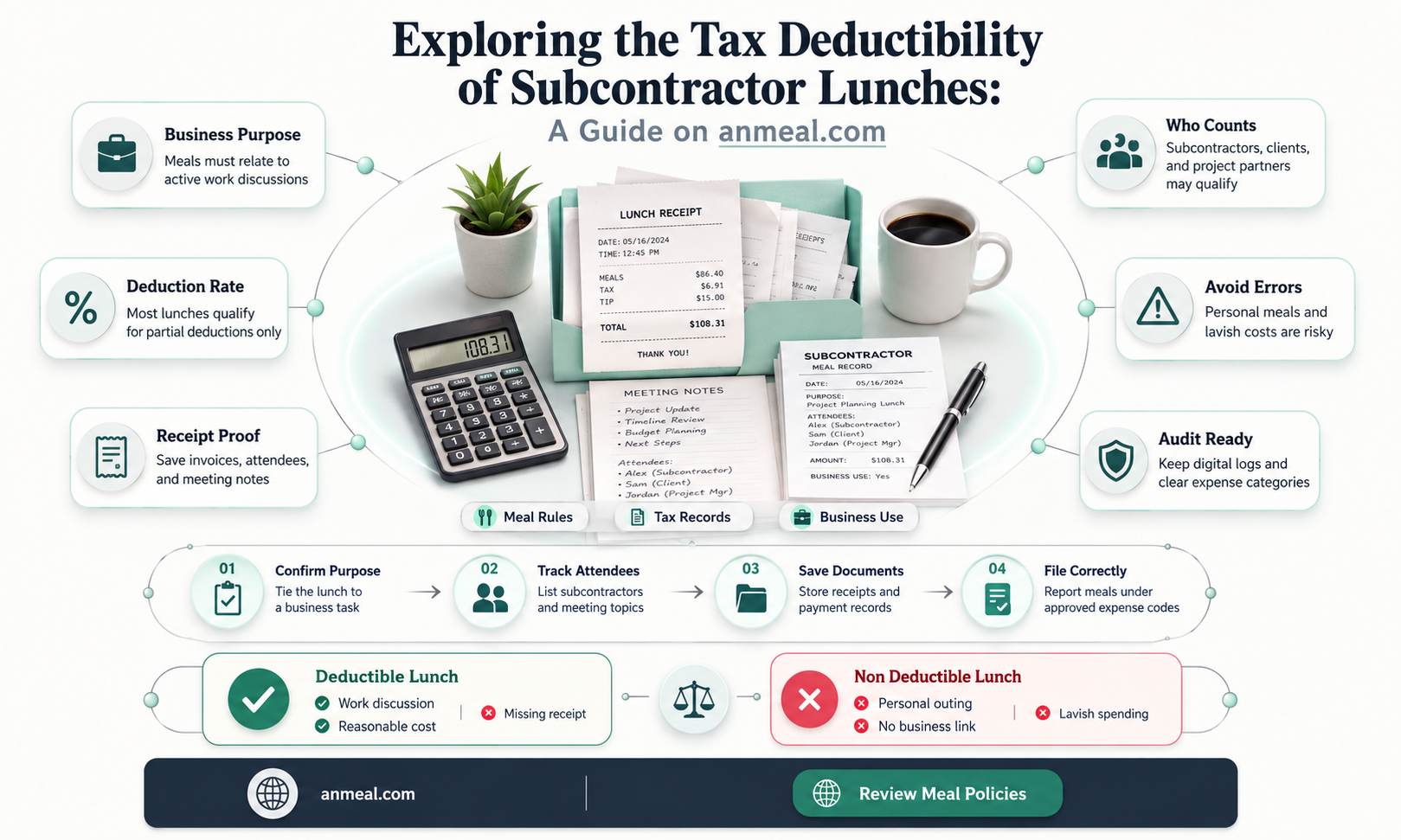

What You'll Learn

- General Rule: Subcontractor lunches are generally not deductible as they are considered personal expenses

- Business Purpose: If the lunch serves a clear business purpose, such as discussing project details, it may be deductible

- Documentation: Keeping detailed records of the business purpose and expenses is crucial for deduction eligibility

- IRS Guidelines: The IRS has specific rules regarding meal deductions, including the 50% limitation for business-related meals

- Exceptions: Certain exceptions apply, such as meals provided for the convenience of the employer or during travel

![]()

General Rule: Subcontractor lunches are generally not deductible as they are considered personal expenses

Generally, subcontractor lunches are not deductible as they are considered personal expenses. This rule stems from the fact that meals are typically seen as a personal benefit rather than a business necessity. However, there are certain circumstances where a subcontractor's lunch expenses may be deductible. For instance, if the subcontractor is traveling for business and the meal is an integral part of the travel, such as a meal during a long drive or while waiting for a flight, it may be considered a deductible travel expense.

Another exception to this general rule is when the subcontractor is attending a business meeting or event where the meal is provided as part of the event. In this case, the meal expense may be deductible as it is directly related to the business activity. It's important to note that the subcontractor must be able to provide documentation to support the business purpose of the meal expense in order for it to be deductible.

Additionally, if the subcontractor is working on a project that requires them to be on-site for an extended period of time, and they are unable to return home for meals, the cost of their meals may be deductible as a necessary business expense. Again, proper documentation is key to ensuring that these expenses are deductible.

In summary, while subcontractor lunches are generally not deductible as they are considered personal expenses, there are certain circumstances where they may be deductible if they are directly related to business activities or travel. It's important for subcontractors to keep accurate records of their meal expenses and to consult with a tax professional to determine what expenses may be deductible in their specific situation.

Crispy Nuggets, Happy Lunch: Tips to Keep Them Dry

You may want to see also

Explore related products

![]()

Business Purpose: If the lunch serves a clear business purpose, such as discussing project details, it may be deductible

To determine if subcontractor lunches are deductible, it's crucial to establish a clear business purpose for the meal. This means the lunch should serve a specific professional objective, such as discussing project details, negotiating terms, or reviewing performance. Without a well-defined business purpose, the IRS may view the meal as a personal expense, which would not be deductible.

When evaluating the business purpose of a subcontractor lunch, consider the following factors: the nature of the discussion, the participants involved, and the documentation available. The discussion should be focused on professional matters related to the subcontractor's work, such as project timelines, deliverables, or invoicing. The participants should be individuals directly involved in the project or contract, such as project managers, team leaders, or financial representatives. Documentation, such as meeting agendas, minutes, or follow-up emails, can help substantiate the business purpose of the lunch.

It's also important to note that the business purpose must be the primary reason for the meal. If the lunch is primarily social or recreational, with only a cursory discussion of business matters, it may not be deductible. The IRS looks closely at the substance of the meeting, not just the form, so it's essential to ensure that the business purpose is genuine and meaningful.

In addition, consider the frequency and timing of subcontractor lunches. If lunches are held regularly or at specific intervals, such as weekly or monthly, it may be easier to establish a pattern of business purpose. However, if lunches are held sporadically or only when convenient, it may be more challenging to demonstrate a consistent business purpose.

Finally, remember that the rules for deducting subcontractor lunches can vary depending on the specific circumstances and the tax laws in your jurisdiction. It's always a good idea to consult with a tax professional or accountant to ensure that you're following the correct guidelines and maximizing your deductions appropriately.

Understanding California Labor Laws: Are Lunches Paid?

You may want to see also

Explore related products

![]()

Documentation: Keeping detailed records of the business purpose and expenses is crucial for deduction eligibility

Maintaining meticulous documentation is the cornerstone of ensuring that subcontractor lunches are deductible. This involves keeping detailed records of the business purpose behind each meal, as well as the associated expenses. The IRS requires clear evidence that the meals are directly related to the business and are not personal expenses. This can be achieved by including information such as the date, location, attendees, and the specific business discussion or activity that took place during the meal.

One effective method of documentation is to use a meal expense log or template. This should include fields for the date, location, attendees, business purpose, and the amount spent. Supporting receipts or invoices should also be attached to the log. For digital records, it's important to ensure that the files are properly labeled and stored in a secure location for easy access in case of an audit.

In addition to the meal expense log, it's crucial to have a clear understanding of the IRS guidelines regarding meal deductions. The IRS allows deductions for meals that are considered "ordinary and necessary" business expenses. This means that the meals must be reasonable in cost and directly related to the business. Lavish or extravagant meals are not deductible, even if they are business-related.

To further substantiate the business purpose of the meals, it's a good practice to schedule meetings or discussions during the meal. This can help to ensure that the meal is not seen as a personal expense, but rather as a necessary part of conducting business. It's also important to note that meals with clients or customers are generally more deductible than meals with employees, as they are more likely to be directly related to generating revenue.

In conclusion, proper documentation is key to ensuring that subcontractor lunches are deductible. By keeping detailed records of the business purpose and expenses, and by following IRS guidelines, businesses can maximize their deductions and minimize the risk of audits or penalties.

Gracefully Declining Lunch with Your Boss: A Guide to Professional Boundaries

You may want to see also

Explore related products

![]()

IRS Guidelines: The IRS has specific rules regarding meal deductions, including the 50% limitation for business-related meals

The IRS has established clear guidelines regarding meal deductions, particularly emphasizing the 50% limitation for business-related meals. This rule is crucial for taxpayers to understand, as it directly impacts the deductibility of meal expenses incurred during business activities. The 50% limitation applies to meals consumed during business meetings, client entertainment, or other work-related events. It's important to note that this rule is not retroactive; it applies to meals consumed after the enactment of the Tax Cuts and Jobs Act in 2017.

One key aspect of the IRS guidelines is the requirement for substantiation. Taxpayers must maintain adequate records to prove the business purpose of the meal, the amount spent, and the date and location of the meal. This can include receipts, credit card statements, or a detailed log of the meal's circumstances. Failure to provide sufficient documentation can result in the disallowance of the deduction.

The IRS also provides exceptions to the 50% limitation for certain types of meals. For example, meals provided to employees on the employer's premises for the convenience of the employer are fully deductible. Additionally, meals consumed while traveling for business are subject to the 50% limitation, but taxpayers can deduct the full cost of meals if they are away from home overnight.

Another important consideration is the distinction between business and personal meals. The IRS scrutinizes the purpose of the meal to determine if it is primarily business-related. If a meal is considered to have a personal component, such as a family member accompanying the taxpayer, the deduction may be disallowed or reduced. Taxpayers should be cautious when claiming meal deductions and ensure that the primary purpose of the meal is business-related.

In conclusion, understanding the IRS guidelines on meal deductions is essential for taxpayers to maximize their deductions while remaining compliant with tax laws. The 50% limitation for business-related meals is a significant rule that requires careful attention to detail and proper documentation. By following these guidelines, taxpayers can avoid potential penalties and ensure that their meal expenses are accurately reported and deducted.

Effortless Lunch Ideas: Quick, Easy, and Delicious Meals

You may want to see also

![]()

Exceptions: Certain exceptions apply, such as meals provided for the convenience of the employer or during travel

In the realm of tax deductions, the rules surrounding subcontractor lunches can be quite nuanced. While the general principle may seem straightforward, there are several exceptions that can muddy the waters. One such exception pertains to meals provided for the convenience of the employer or during travel. This particular exception is crucial for businesses to understand, as it can significantly impact their tax liabilities and financial planning.

To delve into this exception, let's consider a scenario: a construction company hires a subcontractor to work on a project site that is located several hours away from the subcontractor's home. The construction company provides the subcontractor with a daily meal allowance to cover the cost of lunch during the workday. In this case, the meal allowance would likely be considered a deductible business expense, as it is provided for the convenience of the employer (the construction company) and is directly related to the subcontractor's work on the project.

However, it's important to note that this exception is not a blanket rule. There are specific criteria that must be met in order for the meal expenses to be deductible. For instance, the meals must be provided during the subcontractor's normal working hours, and they must be directly related to the performance of the subcontractor's duties. Additionally, the meal expenses must be reasonable and not excessive. If these criteria are not met, the meal expenses may not be deductible, and the business could face potential tax penalties.

Another aspect of this exception to consider is the documentation requirements. In order to claim a deduction for subcontractor meals, the business must maintain accurate and detailed records of the meal expenses. This includes keeping track of the date, time, location, and amount of each meal, as well as the subcontractor's name and the nature of the work being performed. Failure to maintain proper documentation could result in the deduction being disallowed by the tax authorities.

In conclusion, while the exception for meals provided for the convenience of the employer or during travel can be a valuable tax deduction for businesses, it is essential to understand the specific rules and criteria that apply. By doing so, businesses can ensure that they are in compliance with the tax laws and can take advantage of this deduction to reduce their tax liabilities.

Exploring Lunchly's Journey: From Concept to Market Launch

You may want to see also

Frequently asked questions

Generally, yes. Subcontractor lunches can be deducted as a business expense if they meet the IRS criteria for deductibility, which includes being ordinary and necessary for the business.

The IRS criteria for deducting subcontractor lunches include that the expense must be ordinary and necessary for the business. This means the lunch should be a common business practice and directly related to the business's operations.

To document subcontractor lunches for tax deduction purposes, you should keep receipts and records that include the date, amount, location, and business purpose of the lunch.

Yes, there are limits. The IRS allows you to deduct only the amount that is ordinary and necessary. Excessive or lavish expenses may not be deductible.

It depends. If the lunches are not directly related to a specific project but are still necessary for the overall conduct of your business, they may be deductible. However, it's important to document the business purpose to support the deduction.