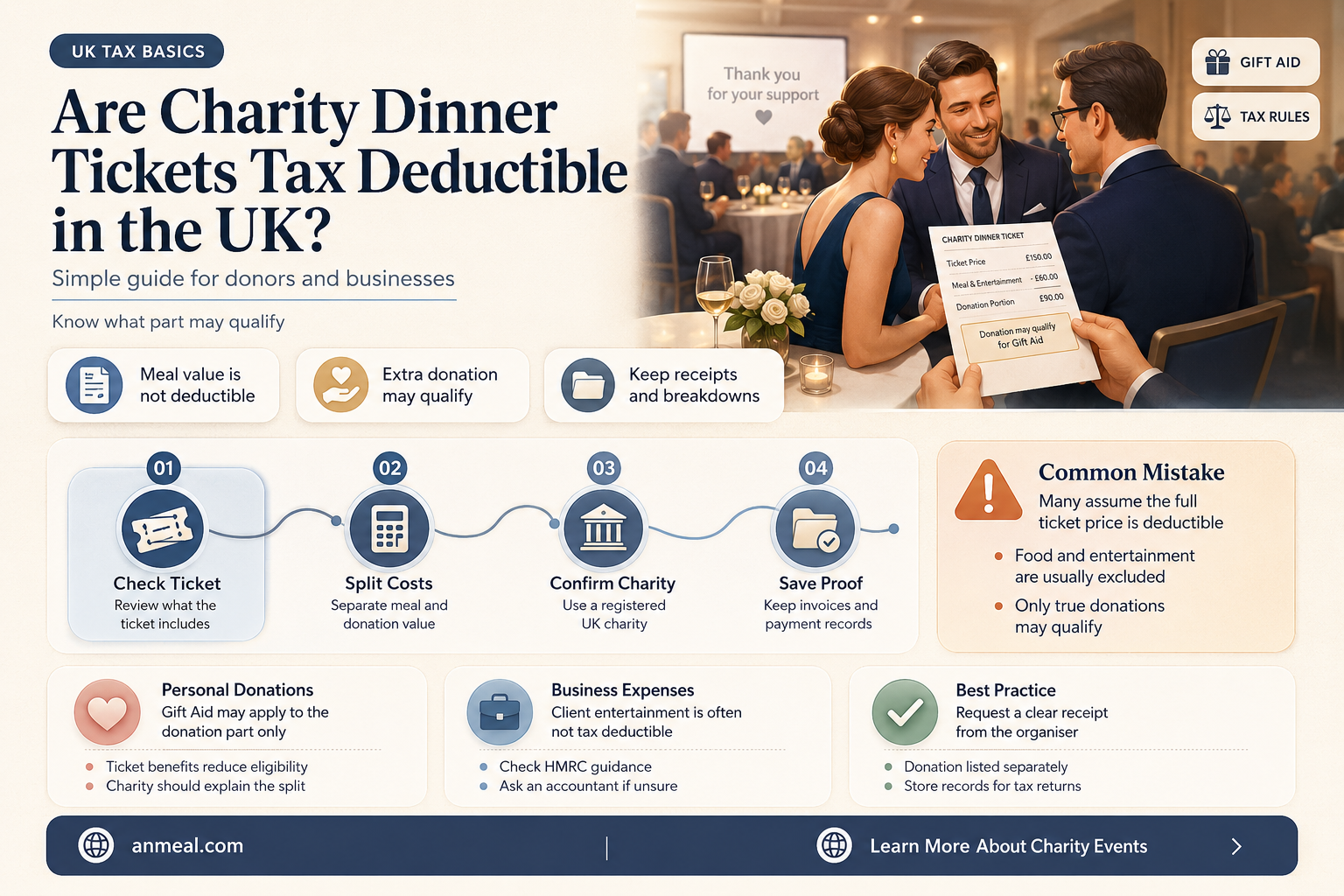

In the UK, determining whether tickets to a charity dinner are tax deductible can be complex, as it largely depends on the nature of the event and the taxpayer's circumstances. Generally, if the ticket price is considered a donation and the event primarily serves a charitable purpose, with minimal private benefit to the attendee, it may qualify for tax relief under Gift Aid. However, if the ticket includes significant non-charitable elements, such as a lavish meal or entertainment, HM Revenue and Customs (HMRC) may view it as a payment for services rather than a donation, making it non-deductible. Businesses may also claim tax relief on charitable donations, but the rules differ, requiring careful documentation and adherence to HMRC guidelines. Always consult a tax professional or refer to HMRC’s guidance to ensure compliance and maximize potential tax benefits.

| Characteristics | Values |

|---|---|

| Tax Deductibility | Generally, tickets to a charity dinner are not tax deductible in the UK. |

| Reason | The cost is considered a payment for a benefit (the meal and event) rather than a pure donation. |

| Exception | If the ticket price exceeds the value of the benefit received (e.g., the meal), the excess amount may be considered a donation and could be tax deductible. |

| Gift Aid | If the charity treats the excess as a donation and the donor is a UK taxpayer, Gift Aid can be claimed on that portion. |

| Documentation | The charity must provide a clear breakdown of the ticket price, separating the donation portion from the benefit value. |

| HMRC Guidance | HMRC states that payments for goods or services (like a charity dinner) are not charitable donations for tax purposes. |

| Donation-Only Events | Events where attendees pay a donation without receiving any benefit (e.g., a virtual event) may be fully tax deductible. |

| Corporate Sponsorship | Businesses may claim tax relief on sponsorship payments if they meet specific criteria, but this is distinct from individual ticket purchases. |

| Advice | Individuals should consult HMRC or a tax advisor for specific circumstances regarding tax deductibility. |

Explore related products

What You'll Learn

- Eligibility Criteria: Conditions for claiming tax relief on charity dinner ticket purchases in the UK

- Gift Aid Rules: How Gift Aid affects tax deductions for charity event tickets

- Business vs. Personal: Tax treatment differences for business and personal ticket purchases

- HMRC Guidelines: Official HMRC rules on deducting charity dinner expenses from taxable income

- Documentation Needed: Required receipts and records to claim tax relief for charity tickets

![]()

Eligibility Criteria: Conditions for claiming tax relief on charity dinner ticket purchases in the UK

In the UK, claiming tax relief on charity dinner ticket purchases isn’t automatic. The eligibility hinges on whether the payment exceeds the value of benefits received. For instance, if a £200 ticket includes a £50 meal, only the £150 donation portion qualifies for relief. HMRC scrutinizes the event’s structure to ensure the primary purpose is charitable, not entertainment. This distinction is critical, as purely social events rarely meet the criteria.

To claim relief, individuals must exceed the £130 annual Gift Aid threshold or donate through payroll giving. Higher-rate taxpayers (40% or 45%) can reclaim the difference between their tax rate and the basic rate (20%) on eligible donations. For example, a £150 donation allows a 40% taxpayer to reclaim £37.50 (£150 * 20% = £30, £150 * 40% = £60, difference = £30). Self-assessment taxpayers can adjust their tax return, while payroll givers benefit automatically.

Businesses face stricter rules. Donations must be made under Gift Aid or through approved schemes like the Cultural Gifts Scheme. The event must be explicitly charitable, with promotional material clearly stating the donation amount. For example, a corporate table costing £1,000 with £700 allocated to charity can claim relief on the £700, provided proper documentation is retained. Failure to separate the donation from the benefit value risks rejection.

Practical tips include requesting a breakdown of ticket costs from the charity and ensuring Gift Aid declarations are completed. Retain all receipts and event literature, as HMRC may audit claims. For higher-rate taxpayers, reclaiming relief via self-assessment is straightforward but often overlooked. Charities should structure events to maximize deductible portions, such as offering a "benefit-free" ticket option, ensuring broader eligibility for attendees.

In summary, eligibility for tax relief on charity dinner tickets requires a clear separation of donation and benefit, adherence to Gift Aid rules, and proper documentation. Both individuals and businesses must navigate these conditions carefully to maximize relief while complying with HMRC guidelines.

Delicious Dinner Pairings: What to Serve with Broccoli for a Balanced Meal

You may want to see also

Explore related products

![]()

Gift Aid Rules: How Gift Aid affects tax deductions for charity event tickets

In the UK, the tax treatment of charity dinner tickets hinges on whether the event offers a benefit to the attendee. Gift Aid, a scheme allowing charities to reclaim tax on donations, complicates this further. If the ticket price primarily covers the cost of the dinner (e.g., venue, food, entertainment), it’s considered a payment for goods or services, not a donation. However, if the ticket price exceeds the event’s cost and the excess is given freely as a donation, Gift Aid can apply. For example, if a £150 ticket includes £100 for the dinner and £50 as a donation, the £50 can qualify for Gift Aid, provided the donor completes a Gift Aid declaration.

To leverage Gift Aid effectively, charities must clearly separate the donation portion from the event cost. This requires transparent communication with attendees. For instance, the invitation should explicitly state the value of the benefit (e.g., "The event cost is £100, and any amount above this is a donation eligible for Gift Aid"). Charities must also ensure donors meet Gift Aid criteria: they must be UK taxpayers and have paid sufficient tax to cover the amount reclaimed by the charity. Failure to meet these conditions can result in complications, such as donors being liable for the tax shortfall.

A practical tip for charities is to use tiered ticketing. For example, offer a £100 "event-only" ticket and a £150 "supporter ticket," where £50 is a donation. This structure simplifies compliance and encourages higher contributions. Donors benefit too, as their donation increases the charity’s income without additional cost to them, thanks to the reclaimed tax. However, charities must keep meticulous records, including Gift Aid declarations and benefit values, to avoid HMRC scrutiny.

Comparatively, events where no benefit is provided (e.g., virtual fundraisers) allow the entire ticket price to qualify for Gift Aid. This highlights the importance of event design in maximising tax efficiency. For charity dinners, the key is balancing attendee experience with compliance. While Gift Aid can significantly boost funds, it requires careful planning and transparency. Ultimately, understanding these rules ensures both charities and donors maximise the impact of their contributions while staying within legal boundaries.

Post-Shabbat Cleanup: Who Handles the Mess After Dinner?

You may want to see also

Explore related products

![]()

Business vs. Personal: Tax treatment differences for business and personal ticket purchases

In the UK, the tax treatment of charity dinner tickets hinges critically on whether the purchase is classified as a business or personal expense. For businesses, tickets can be tax-deductible if the event directly relates to the company’s trade or profession. For instance, if a company purchases tickets to network with potential clients or strengthen business relationships, HMRC may allow the cost to be claimed as a legitimate business expense, reducing taxable profits. However, the event must serve a clear business purpose; purely social or charitable intentions without a commercial angle will not qualify.

Contrastingly, personal ticket purchases for charity dinners are not tax-deductible. Individuals cannot claim relief on their self-assessment tax returns for such expenses, even if the event supports a worthy cause. The rationale is straightforward: personal donations, while commendable, are not considered a business expense and thus do not qualify for tax relief. However, individuals can still benefit indirectly if the charity claims Gift Aid on their donation, allowing the charity to reclaim basic-rate tax from HMRC.

A key distinction lies in the intent and documentation. Businesses must maintain clear records demonstrating the commercial purpose of the ticket purchase, such as meeting minutes, correspondence with clients, or follow-up actions. Without such evidence, HMRC may reclassify the expense as non-deductible. For personal purchases, no such documentation is required, but individuals should be aware that claiming tax relief on these tickets would be incorrect and could lead to penalties.

Practical tip: If a business owner attends a charity dinner with both personal and business intentions, it’s advisable to allocate the cost proportionally. For example, if 70% of the event’s purpose is business-related (networking, client meetings), only that portion of the ticket cost should be claimed as a business expense. This approach ensures compliance with HMRC rules while maximising legitimate deductions.

In summary, the tax treatment of charity dinner tickets in the UK is starkly different for businesses and individuals. Businesses can claim deductions if the expense is directly linked to their trade, but personal purchases remain non-deductible. Understanding this distinction and maintaining proper documentation is essential to avoid errors and maximise tax efficiency.

Top Franschhoek Dinner Spots: A Culinary Journey in Wine Country

You may want to see also

Explore related products

![]()

HMRC Guidelines: Official HMRC rules on deducting charity dinner expenses from taxable income

In the UK, the tax treatment of charity dinner expenses hinges on whether the payment is a genuine donation or includes a benefit to the donor. HMRC guidelines are clear: for a payment to qualify as a tax-deductible donation, it must be made without receiving anything in return. If the ticket price covers a meal, entertainment, or other perks, the portion of the payment attributable to these benefits is not deductible. Only the amount that exceeds the value of the benefits received can be claimed as a charitable donation.

Consider a charity dinner ticket priced at £200, where £150 covers the meal and £50 is a direct donation. In this scenario, only the £50 is eligible for tax relief. To simplify compliance, some charities issue split receipts, clearly separating the donation from the cost of benefits. Donors should request such documentation to ensure accurate claims. For businesses, the rules differ slightly: while the donation portion remains deductible, the cost of the meal and entertainment may be subject to additional restrictions under corporate entertaining rules.

HMRC also emphasizes the importance of the charity’s status. Tax relief is only available if the donation is made to a registered UK charity or a recognized international charitable organization. Donations to non-charitable organizations, even if they have a charitable purpose, do not qualify. Individuals can claim tax relief through Gift Aid, which allows the charity to reclaim basic rate tax on the donation, or through self-assessment if they are higher or additional rate taxpayers.

A practical tip for maximizing tax efficiency is to consider "Gift Aid It" schemes, where the charity can reclaim 25p for every £1 donated at no extra cost to the donor. Higher rate taxpayers can then claim back the difference between the higher rate of tax and the basic rate on their self-assessment return. For example, a £100 donation with Gift Aid allows the charity to claim £25, and a higher rate taxpayer can claim back £25 (£100 x 20%) on their tax return.

In summary, while charity dinner tickets can offer tax benefits, careful scrutiny of the payment structure is essential. Donors must ensure the charity provides clear documentation separating the donation from the cost of benefits. By adhering to HMRC guidelines and leveraging schemes like Gift Aid, individuals and businesses can support charitable causes while optimizing their tax position. Always consult the latest HMRC guidance or a tax professional for specific advice tailored to your circumstances.

Sunday Dinner Time: When to Serve the Perfect Weekend Meal

You may want to see also

Explore related products

![]()

Documentation Needed: Required receipts and records to claim tax relief for charity tickets

To claim tax relief for charity dinner tickets in the UK, meticulous documentation is essential. HM Revenue & Customs (HMRC) requires clear proof that the payment qualifies as a charitable donation, not merely an expense for personal benefit. The cornerstone of this proof is the receipt, which must explicitly state the charity’s name, registration number, and the amount donated. If the ticket includes a non-donation element (e.g., meal cost), the receipt must differentiate between the donation and the benefit received. Without this breakdown, the entire amount may be ineligible for relief.

Beyond receipts, maintaining detailed records is equally critical. For individuals, this includes keeping a record of the event date, the charity’s purpose, and any correspondence confirming the donation. For businesses, additional documentation such as meeting minutes approving the donation or invoices linked to the payment may be necessary. These records serve as a safeguard during HMRC audits, ensuring the claim’s legitimacy. A common oversight is failing to retain these documents for the required six years, which can lead to disallowed claims or penalties.

A practical tip for ensuring compliance is to request a formal acknowledgment from the charity. This document should confirm the donation amount, the event’s charitable purpose, and that no significant benefit was received in return. For example, if a £200 ticket includes a £50 meal, the acknowledgment should state that £150 was donated. This clarity not only strengthens the claim but also aligns with HMRC’s guidelines on “benefit thresholds,” which limit the value of benefits received relative to the donation.

Comparatively, while individuals can claim tax relief through Gift Aid or self-assessment, businesses must ensure the donation aligns with their corporate objectives and is reported in financial statements. For instance, a company donating £1,000 worth of tickets must include this in their Corporation Tax return, supported by receipts and acknowledgments. Failure to do so can result in the donation being treated as taxable income, negating any relief.

In conclusion, claiming tax relief for charity dinner tickets hinges on precise documentation. Receipts must clearly separate donations from benefits, while records should provide a comprehensive audit trail. By adhering to these requirements and leveraging practical strategies like obtaining formal acknowledgments, individuals and businesses can confidently navigate HMRC’s rules, maximizing their tax relief while supporting charitable causes.

Exploring Omakase: The Art of Chef-Curated Japanese Dining Experience

You may want to see also

Frequently asked questions

Yes, tickets to a charity dinner can be tax deductible in the UK if the event is organised by a registered charity and the payment qualifies as a donation.

The tax-deductible portion is the amount paid above the value of the benefit received (e.g., the meal or entertainment). If the ticket price is purely a donation, the full amount may be deductible.

Yes, if the ticket price qualifies as a donation and you make a Gift Aid declaration, the charity can reclaim tax on your contribution, increasing its value.

Yes, businesses can claim tax relief on charitable donations, including tickets to charity dinners, as long as the event is organised by a registered charity and the payment is not for a personal benefit.

You’ll need a receipt or acknowledgment from the charity confirming the donation amount and, if applicable, a Gift Aid declaration to support your tax relief claim.