Working lunches can be a common perk offered by employers, but they often raise questions regarding their tax implications. In many jurisdictions, the taxability of working lunches depends on various factors, including the nature of the meal, the venue, and the business purpose behind the lunch. Typically, if a working lunch is held for a legitimate business reason and the expenses are reasonable, they may be considered tax-deductible for the employer and tax-free for the employee. However, if the lunch is seen as a form of compensation or lacks a clear business purpose, it could be subject to taxation. It's essential for both employers and employees to understand the specific tax laws and regulations in their region to ensure compliance and avoid unexpected tax liabilities.

| Characteristics | Values |

|---|---|

| Definition | Working lunches refer to meals provided to employees during their workday, typically when they are required to work through their usual meal break. |

| Taxability | In many jurisdictions, working lunches are considered a taxable benefit because they are provided in lieu of compensation. |

| Exceptions | Some countries or regions may have specific exceptions or rules that apply to working lunches, such as if they are provided for the convenience of the employer or if they are customary in the industry. |

| Valuation | The taxable value of working lunches is often determined by the fair market value of the meal or the amount the employer pays for it. |

| Reporting | Employers are typically required to report the taxable value of working lunches on the employee's pay stub or tax forms. |

| Employee Impact | Employees may need to pay income tax on the taxable value of working lunches, which could affect their overall compensation and tax liability. |

| Employer Impact | Employers may need to withhold taxes on the taxable value of working lunches and report this information to tax authorities. |

| Compliance | It is important for both employers and employees to understand and comply with the tax laws and regulations related to working lunches to avoid penalties or fines. |

| Documentation | Keeping accurate records of working lunches, including the date, time, location, and value of the meal, can help with tax reporting and compliance. |

| Consultation | Employers and employees may want to consult with a tax professional or refer to official tax guidance to ensure they are correctly handling the tax implications of working lunches. |

Explore related products

What You'll Learn

![]()

Definition of taxable benefits

Taxable benefits are a crucial aspect of employment compensation that can have significant implications for both employers and employees. These benefits are typically provided by employers to employees in addition to their regular salary or wages and are subject to taxation. Understanding what constitutes a taxable benefit is essential for accurate tax reporting and compliance with relevant tax laws.

In the context of working lunches, it is important to determine whether such meals are considered taxable benefits. Generally, a working lunch is a meal provided to an employee during their workday, often for the purpose of conducting business or fostering team relationships. To ascertain whether a working lunch is taxable, one must consider the specific circumstances under which it is provided.

For instance, if an employer provides a working lunch as a regular part of an employee's compensation package, it is likely to be considered a taxable benefit. This is because it represents a form of additional compensation that is provided in lieu of cash. However, if a working lunch is provided on an occasional basis for specific business purposes, such as a client meeting or a team-building event, it may not be considered a taxable benefit.

The key factors in determining the taxability of working lunches include the frequency with which they are provided, the purpose of the meal, and the value of the benefit. Employers should carefully consider these factors when deciding whether to provide working lunches and how to report them for tax purposes. Employees, on the other hand, should be aware of the potential tax implications of receiving working lunches and ensure that they are properly reported on their tax returns.

In conclusion, the definition of taxable benefits is a complex area of tax law that requires careful consideration of various factors. Working lunches can be considered taxable benefits depending on the circumstances under which they are provided. Employers and employees should consult with tax professionals to ensure that they are in compliance with relevant tax laws and regulations.

Navigating the Process: Filing for Reduced Lunch at Reeths Puffer

You may want to see also

Explore related products

![]()

Employer-provided meals

Employers often provide meals to their employees as a perk or incentive, but this practice can have tax implications. In many jurisdictions, employer-provided meals are considered a taxable benefit, meaning that the value of the meals must be reported as income and taxed accordingly. This can be a surprise to both employers and employees who may not be aware of the tax rules surrounding this type of benefit.

One common scenario where employer-provided meals may be taxable is when an employer offers free or subsidized meals to employees in a cafeteria or dining facility on the company premises. This type of benefit is often provided to encourage employees to stay on-site during their lunch break and to promote a sense of community within the workplace. However, the tax authorities may view this as a form of compensation, and therefore subject to taxation.

Another situation where employer-provided meals may be taxable is when an employer provides meals to employees during business travel or at company events. While these meals may be necessary for the conduct of business, they are still considered a taxable benefit if they are provided by the employer. This is because the meals are not considered a direct business expense, but rather a personal expense that is being reimbursed by the employer.

To avoid unexpected tax liabilities, employers should be aware of the tax rules surrounding employer-provided meals and take steps to comply with these rules. This may include reporting the value of the meals on employees' pay stubs or W-2 forms, and withholding the appropriate amount of tax. Employers may also want to consider alternative ways to provide meals to employees, such as through a tax-free reimbursement arrangement or by offering meal vouchers that can be used at a variety of restaurants.

In conclusion, while employer-provided meals can be a valuable perk for employees, they can also have tax implications that both employers and employees should be aware of. By understanding the tax rules surrounding this type of benefit and taking steps to comply with these rules, employers can avoid unexpected tax liabilities and ensure that their employees are not caught off guard by additional taxes on their income.

Unveiling the Truth: Lunchly's Cheese Controversy Explored

You may want to see also

Explore related products

![]()

Working lunch criteria

To determine whether working lunches are a taxable benefit, it's essential to understand the specific criteria that define a working lunch. A working lunch is typically a meal taken during the workday where the employee is engaged in business-related activities. This can include meetings with clients, discussions with colleagues, or any other work-related tasks that occur during the meal.

One key criterion is that the lunch must be directly related to the employee's job duties. This means that the meal should be a necessary part of the workday, rather than a personal or leisure activity. For example, if an employee takes a lunch break to run personal errands or meet with friends, this would not qualify as a working lunch.

Another important factor is the timing of the lunch. A working lunch should occur during the employee's regular working hours. If an employee takes a meal outside of their normal work schedule, it may not be considered a working lunch. Additionally, the duration of the lunch should be reasonable and in line with the employee's usual break times.

The location of the lunch can also play a role in determining whether it's a taxable benefit. If the lunch takes place at the employee's regular workplace, it's more likely to be considered a working lunch. However, if the lunch occurs at a different location, such as a restaurant or a client's office, it may still qualify as long as the other criteria are met.

Finally, the nature of the meal itself should be considered. A working lunch should be a reasonable and modest meal, rather than an extravagant or luxurious one. The cost of the meal should be in line with the employee's usual lunch expenses, and any additional costs, such as tips or gratuities, should be minimal.

In summary, to qualify as a working lunch, the meal must be directly related to the employee's job duties, occur during regular working hours, take place at a reasonable location, and be of a modest nature. By understanding these criteria, employees and employers can better navigate the tax implications of working lunches.

Royal Lunch Crackers: A Nostalgic Comeback or Just a Rumor?

You may want to see also

Explore related products

![]()

Tax implications

In the realm of employee benefits, the tax implications of working lunches can be a complex and often overlooked area. Employers may provide working lunches as a perk to enhance employee satisfaction and productivity, but these benefits can have unintended tax consequences. The IRS considers working lunches to be a form of compensation, which means they are subject to taxation. This can lead to additional income tax liabilities for employees and potential payroll tax obligations for employers.

One key consideration is whether the working lunch is provided as a fringe benefit or as part of an employee's regular compensation. If the lunch is provided as a fringe benefit, it may be taxable to the employee as imputed income. The value of the benefit is typically determined by the fair market value of the meal. Employers must report the value of these benefits on the employee's Form W-2, which can increase the employee's taxable income and potentially push them into a higher tax bracket.

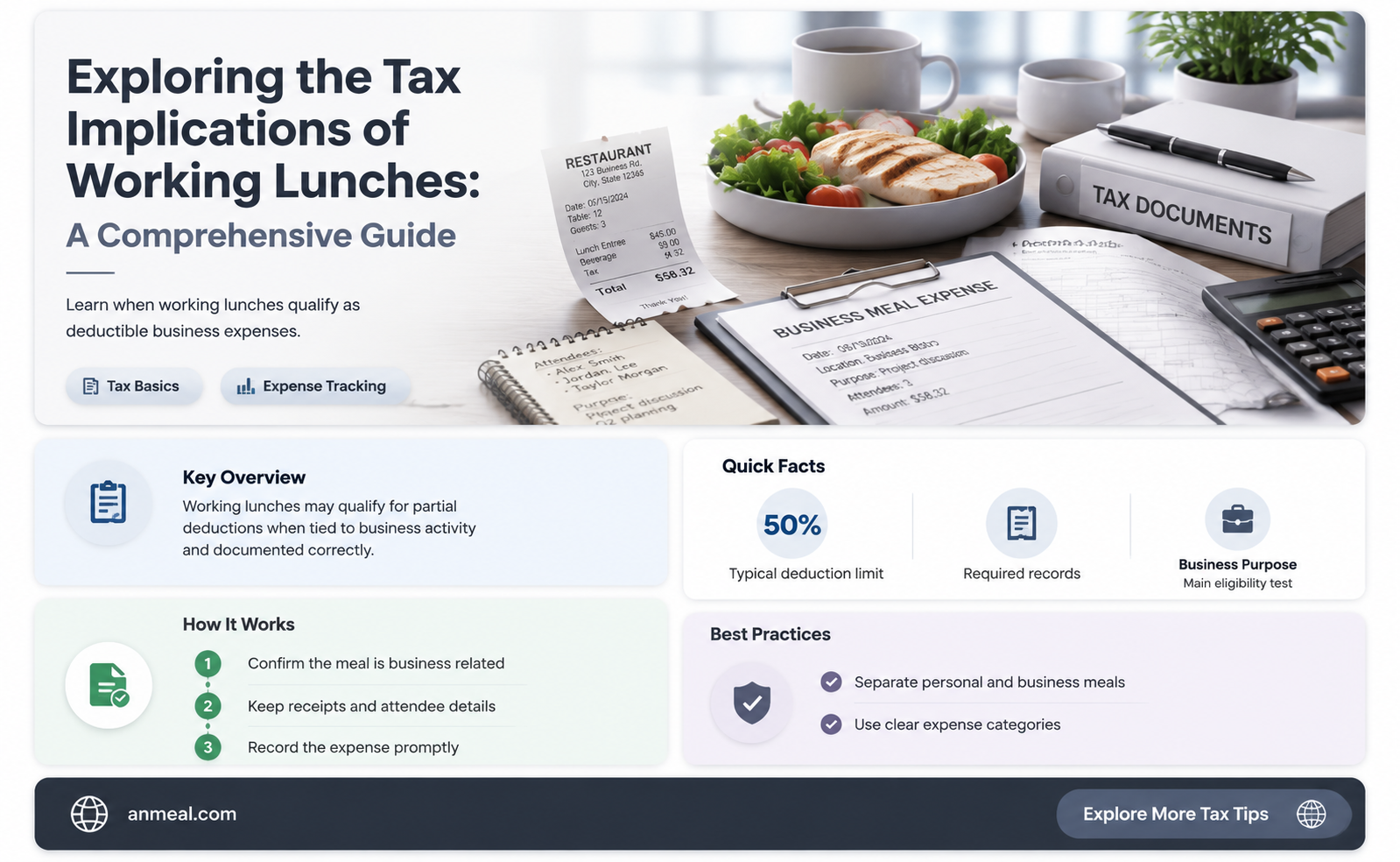

On the other hand, if the working lunch is provided as part of an employee's regular compensation, it may be deductible by the employer as a business expense. However, this deduction is subject to certain limitations and requirements. The meal must be directly related to the conduct of the employer's business, and the employer must maintain adequate records to substantiate the deduction. Additionally, the deduction may be limited by the 50% deduction limit for business meals.

Another important aspect to consider is the potential for working lunches to trigger additional payroll taxes. If the value of the working lunch is considered taxable compensation, it may increase the employee's gross income for payroll tax purposes. This can lead to higher Social Security and Medicare tax liabilities for both the employee and the employer. Employers must ensure that they are properly withholding and reporting these taxes to avoid penalties and interest.

To mitigate the tax implications of working lunches, employers can consider implementing policies that limit the frequency or value of these benefits. They can also explore alternative ways to provide meals, such as through a cafeteria plan or a meal reimbursement program, which may offer more favorable tax treatment. Employees, on the other hand, should be aware of the potential tax consequences of receiving working lunches and may want to consult with a tax professional to understand their individual tax liabilities.

In conclusion, the tax implications of working lunches can be significant and require careful consideration by both employers and employees. By understanding the rules and regulations surrounding these benefits, employers can make informed decisions about how to structure their meal programs to minimize tax liabilities, while employees can take steps to manage their own tax obligations.

Discover Lunchly's Global Reach: Where You Can Find It

You may want to see also

Explore related products

![]()

Employee reporting requirements

Employees are often required to report certain types of benefits received from their employer for tax purposes. In the context of working lunches, this typically involves declaring the value of any free or subsidized meals provided during the workday. The specific reporting requirements can vary depending on the jurisdiction and the employer's policies, but generally, employees must keep accurate records of the dates, times, and values of any working lunches they receive.

One common method for reporting working lunches is through the employer's payroll system. Employees may be required to submit a form or log detailing their meal expenses, which the employer will then use to calculate the appropriate tax withholding. In some cases, employees may also need to provide receipts or other documentation to support their claims.

It's important for employees to understand their reporting obligations to avoid potential tax penalties or other consequences. Failure to report working lunches accurately can lead to underpayment of taxes, which may result in fines or interest charges. Additionally, some employers may have their own policies regarding the reporting of working lunches, and failure to comply with these policies could lead to disciplinary action or other repercussions.

To ensure compliance with reporting requirements, employees should familiarize themselves with their employer's policies and procedures regarding working lunches. They should also keep accurate records of their meal expenses and submit any required forms or documentation in a timely manner. By taking these steps, employees can help ensure that they are meeting their tax obligations and avoiding any potential penalties or consequences.

Can Teachers Check My Child's Lunch? Understanding School Policies

You may want to see also

Frequently asked questions

Generally, working lunches are not considered a taxable benefit if they meet certain criteria. They must be occasional, not a regular part of an employee's compensation, and should be directly related to the business.

To be tax-free, a working lunch should be occasional, directly related to the business, and not a regular part of an employee's compensation. It should also be documented properly to substantiate the business purpose.

Working lunches should be documented with details such as the date, location, attendees, business purpose, and expenses incurred. Keeping accurate records helps substantiate the business purpose and ensures compliance with tax regulations.

Yes, if working lunches are provided as a regular part of an employee's compensation package, or if they are not directly related to the business, they may be considered taxable. Additionally, if the lunches are lavish or extravagant, they could be subject to taxation.